Overview

- The 2024-25 Frozen Texas Budget would have kept the state’s budget from growing as it is already too big, thereby excessively burdening taxpayers. This also helps quickly achieve the three-step process to eliminate all property taxes over the next decade by limiting government spending at the state and local levels and returning surplus collected taxpayer dollars to taxpayers.

- The 88th Texas Legislature passed the 2024-25 budget in 2023, which resulted in the largest budget increase and second-largest property tax relief in Texas history after a regular and four special sessions. The 89th Texas Legislature in 2025 must practice better budget restraint to reduce the growing spending burden, sustain past property tax relief efforts, and provide more tax relief.

- Freezing the Texas budget and returning “surplus” money to taxpayers by reducing school district maintenance and operations property tax rates will provide a path to eliminate nearly half of property taxes in Texas. Combining this with spending restraint by local governments and returning “surplus” money to taxpayers by reducing property tax rates will provide a reasonable path to eliminating immoral property taxes that tax unrealized gains in Texas so Texans can have their right to own property.

- See an Overview of the Texas Budget.

Introduction

Recently, the Texas Legislative Budget Board released the Fiscal Size-Up 2024-25 Biennium report with the latest estimated or budgeted amounts in the prior 2022-23 budget and the appropriated 2024-25 budget. The results from the 88th Texas Legislature’s efforts after a regular and four special sessions resulted in the largest budget increase, the largest corporate welfare increase, the largest social safety net increase, and the second largest property tax relief in Texas history.

These results are not what one expects in the red state of Texas, but the appropriate ways to evaluate the latest budget data provided here show much room for fiscal improvements in the Lone Star State. If these efforts last session continue, Texas will not have sustainable budgeting, nor will Texans be as prosperous because of higher taxes, less economic growth, and fewer well-paid jobs. Fortunately, the path forward to achieve fiscal sustainability can happen by at least passing a frozen budget for the next biennium and returning excess collected taxes, called a “surplus,” to taxpayers by reducing school district maintenance and operations (M&O) property tax rates.

The genius of America’s republic with federalism provides laboratories of competition among the states that Texas will not lead if this recent trend of excessive spending continues. Texas can overcome these challenges and provide the fiscally conservative path forward for Texans to benefit and other states, countries, and local governments to follow for maximum human flourishing.

Texas Budget as Reported by the Legislative Budget Board

The Legislative Budget Board comprises elected state officials and staff who evaluate, report, and determine key components of the state’s budget. These components include determining the growth rate of the constitutional spending limit, budget totals for each period to report to the public, and other factors. Unfortunately, the LBB reported the budget figures relatively late, giving the author and other Texans less time to evaluate the budget before the next session, which begins in January 2025.

The amounts in the LBB’s latest report for the 2024-25 budget provide appropriated amounts for that period and expended or budgeted amounts for the previous 2022-23 budget. While the LBB uses these amounts and shares them with legislators to help evaluate budgeting decisions, the amounts have problems.

Problems with Comparisons in the LBB’s Fiscal Size-Up

The primary issue is that the amounts in the 2022-23 budget are not comparable with those in the 2024-25 budget. This is because the 2022-23 budget includes initially appropriated amounts passed in 2021, supplemental appropriated amounts in 2023 to backfill any underfunded programs, and other expenditures during the budget period. However, the 2024-25 budget includes only initially appropriated amounts during 2023 until any supplemental appropriated amounts in 2025 and other expenditures later. This paper addresses this by considering the calculations in the Conservative Texas Budget and Frozen Texas Budget approaches below.

While this is an issue for appropriately comparing the budget over time, the LBB’s approach is useful because it determines the amounts for the constitutional and statutory spending caps when the LBB meets the fall before a regular session. The constitutional spending limit is on certain general revenue not dedicated by the constitution (about 40% of the total budget), and the statutory spending limit covers consolidated general revenue (about 50% of the total budget). The spending growth cap determined by the LBB for the 2024-25 budget was 12.33% based on the average rate of population growth times inflation over the last two fiscal years and the upcoming two fiscal years.

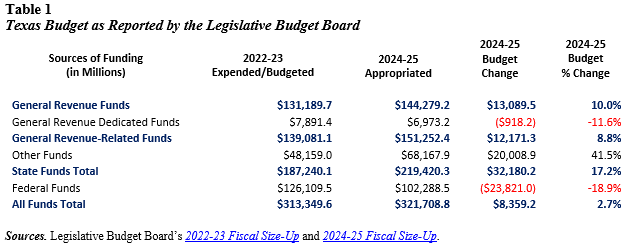

Given this information, we can better understand the LBB’s report, which compares spending to appropriations, which is like comparing apples with oranges and not appropriate accounting. Table 1 provides the budget information from Figures 1 to 14 in the LBB’s report that state officials can claim shows the budget is well below the spending limit. Still, these comparisons are incomplete and need further evaluation.

Even with these calculations, Figure 24 of the LBB’s report shows the available amounts of $16.8 billion under the Constitutional pay-as-you-go limit, $5.1 billion under the Constitutional and statutory tax and spending limit, and $13.8 billion under the statutory consolidated general revenue limit. Given that the data in Table 1 provides an inconsistent apples-to-oranges budget comparison, the tables below are more accurate ways for an apples-to-apples comparison from initial appropriations to initial appropriations.

Consistent Comparisons of the Texas Budget

Any growth in a government’s budget is an expansion of the role of government in our lives, potentially reducing our liberty. But there can be legitimate reasons for the growth of limited government if it preserves liberty by not overburdening taxpayers with funding excessive spending with costly taxes.

Conservative Texas Budget

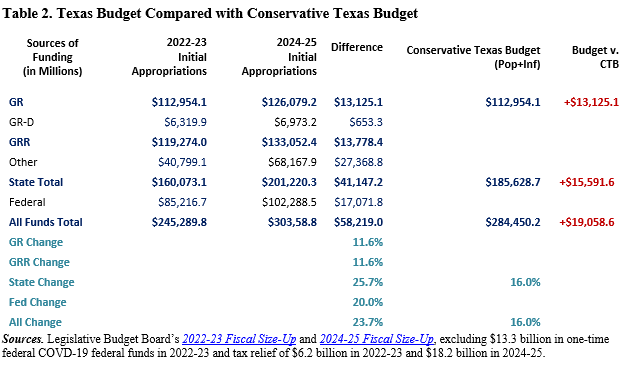

The first comparison is based on a long-held view of fiscal conservatism that the budget should not grow by more than the average taxpayer’s ability to pay for it, as measured by the rate of population growth plus inflation. Limiting a government’s budget growth to this metric essentially freezes the budget in inflation-adjusted per capita terms. This approach has been considered in my research for the Conservative Texas Budget, Sustainable Budget Project, and responsible budget approaches in other states. The Conservative Texas Budget approach uses the rate of population growth plus inflation in the two prior years before 2023 for a biennial spending limit of 16%. This rate is not a target but a maximum, especially considering elevated inflation rates created by the Federal Reserve. excludes tax relief that does not grow the government, including the $6.2 billion in general revenue for the 2022-23 appropriations and $18.2 billion in general revenue for the 2024-25 budget. The property tax relief amount for the 2024-25 budget period is in the budget, SB 2, and HJR 2. This included $5.3 billion to maintain past property tax relief efforts in the budget. It also includes $12.7 billion in new property tax relief through reducing the school district M&O property tax rates by an additional 10.7 cents per $100 valuation, raising the homestead exemption from $40,000 to $100,000, and excluding property tax relief amounts from the Constitutional spending limit. Finally, it includes $600 million to raise the income exemption for businesses to pay franchise taxes to $2.47 million. This approach also excludes $13.3 billion in federal funding for COVID-related relief efforts, as these were one-time funding sources that should not go into ongoing budget items.

Table 2 shows what the Conservative Texas Budget looks like when excluding tax relief and one-time federal funding amounts in initial appropriations in both budget periods.

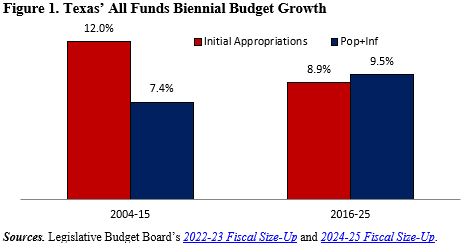

Using the CTB approach above, Figure 1 highlights how the budget has improved since the implementation of the CTB started with the 2016-17 budget. This looked much better before the 2024-25 budget, but the massive growth of the current budget raised the growth of initial appropriations even as the rate of population growth plus inflation rose slightly during the latter five budget period. If the growth of the budget is not controlled, it will soon surpass the rate of population growth plus inflation like it did during the prior six budget periods, which is unsustainable.

While the state’s budget has improved over the last decade compared with rates of population growth plus inflation, the state’s budget is up well above the rates since the 2004-05 budget. The cumulative annual difference above these rates since then is $262.5 billion, meaning a family of four owes, on average, $17,300 more in taxes than otherwise.

Frozen Texas Budget

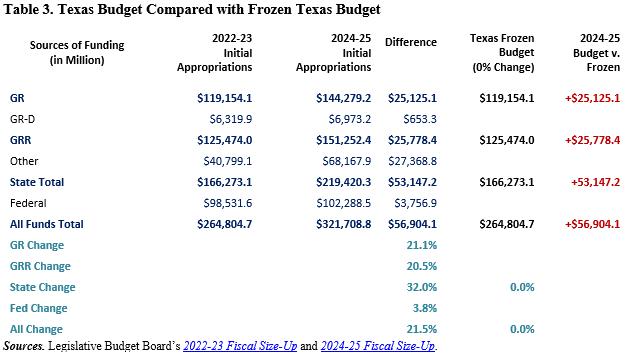

The CTB is an important approach but has limitations because Texas taxpayers are already paying too much for their government. This is a good reason to freeze or even cut the Texas budget. Considering the initial appropriations in 2022-23 and 2024-25, with tax relief and COVID-related funding included in both periods, Table 3 compares the budget with a Frozen Texas Budget.

These increases in initial appropriations to initial appropriations for general funds, general-revenue-related funds, state funds, and all funds are substantial and likely the largest in Texas history, as not all years of Texas history are available. The Legislature provided $12.3 billion in new property tax relief, $600 million in new franchise tax relief, and $5.3 billion to maintain old relief for the 2024-25 budget. This $18.2 billion in tax relief did not grow the government so that it could be removed from these figures, but the $6.2 billion in tax relief in 2022-23 must also be removed for consistency. After removing these tax relief amounts in both budget periods, the increases remained excessive at 25.7% in state funds, like for the CTB above, and 17.4% in all funds, which is different than the CTB because the CTB excludes the $13.3 billion amount for COVID-related federal funds in 2022-23.

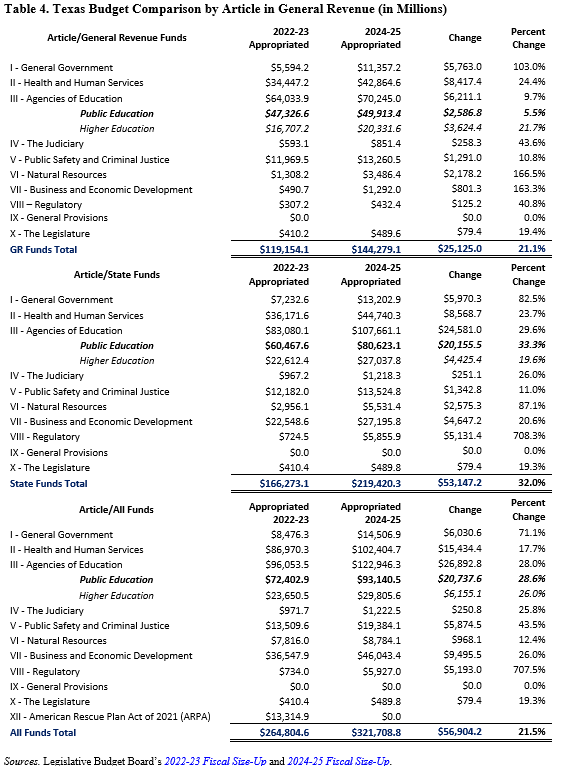

Budget Increases by Article, Including Public Education

With these unsustainable budget increases, it is important to consider where these appropriations are throughout the budget. While some consider declines in funding for public education, also known as government schooling, the amount is up substantially when appropriately considering the Frozen Texas Budget approach. Table 4 shows the increases in initial appropriations for general revenue, state funds, and all funds, respectively, from 2022-23 to 2024-25.

Conclusion

The comparisons above highlight how the LBB’s report is informative but incomplete and misleading as it provides an inconsistent comparison of spending-to-appropriations. By appropriately accounting for appropriations-to-appropriations like the above for the Conservative Texas Budget and Frozen Texas Budget, the increase in the budget is far greater than the average taxpayer can afford to pay for and is well above what is needed to correct past budget excesses. While the LBB shows that general revenue-related funds increased by 8.8% and all funds increased by 2.7%, this inconsistent approach finds that state funds increased by 17.2%. However, the consistent approaches prove that the budget increased by 25.7% in state funds for the CTB, excluding the amounts for tax relief and COVID-related funding, or by 32% for the Frozen Texas Budget, including those amounts. Moreover, the budget increased by 23.7% in all funds for the CTB or by 21.5% for the FTB. Therefore, it is highly likely that when the supplemental appropriations and other expenditures happen during the 2024-25 budget, there can be a consistent spending-to-spending comparison, showing much larger increases in the LBB’s figures that look more similar to the CTB or FTB.

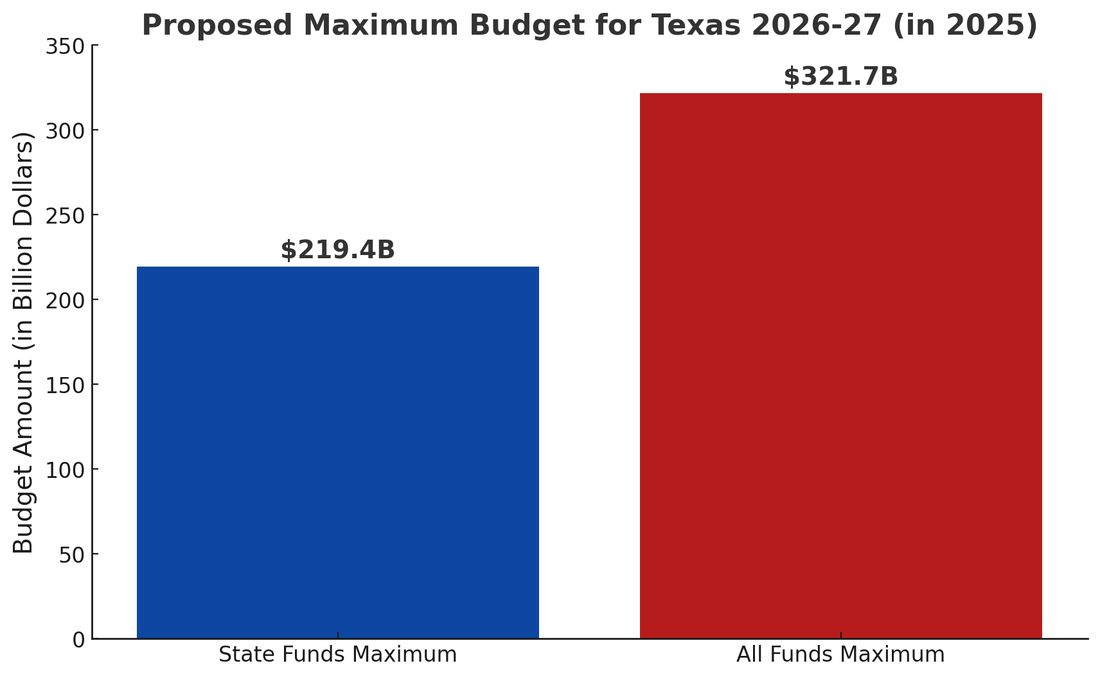

Digging into these budget amounts provides a better understanding that the latest Texas budget is unsustainable and must be corrected in 2025. This is why the Frozen Texas Budget should be the maximum for the 2026-27 budget in 2025, making the maximum amounts appropriated be $219.4 billion in state funds and $321.7 billion in all funds. However, the Texas Legislature should strongly consider substantial cuts in appropriations, given the historic budget increases in the last session. The starting point should be 10% cuts across the board, but 20% cuts should not be out of the question. Recall that the government has no money; every dollar it spends comes from taxpayers. If the government is going to spend more than 20% each biennium like it did last session, Texans have less liberty and less opportunity to flourish.

Places to start cutting would be massive increases in corporate handouts and safety net programs expanded last session. In addition to getting rid of pork, the Legislature should consider replacing the arcane school finance system with funding through universal education savings accounts (ESAs). This approach could substantially reduce expenditures on K-12 schooling from about $17,000 for each of the 5.5 million students in public education to about $12,000 for each of the 6.3 million school-age kids in Texas. This could bring spending on K-12 schooling down from about $93 billion to $75.6 billion per year. These savings should reduce school district maintenance and operations property tax rates to put them on a fast path to elimination. This approach would also better empower every parent with the opportunity to school their kids in a way that best meets their unique needs. It would also help keep more money in their pocket for transportation to schooling, tutoring, books, and more, whether they choose public, private, home, co-op, or other types of schooling. School choice helps empower parents, improve student outcomes, increase teacher pay, and expand economic output.

Finally, according to the latest data from the Comptroller, total property taxes barely decreased by about $345 million last year, or about -0.4% (although their data is missing a dozen school district property tax levies, meaning the amount of property taxes collected in 2023 could be higher than the Comptroller’s Office estimates, likely negating the decline estimate), despite the state appropriating more than $12.7 billion to reduce school district M&O property taxes, by reducing the property tax rate by an additional 10.7 cents per $100 valuation and raising the homestead exemption to $100,000.

In the next session, the Legislature should better limit government spending, reform school finance, and use the “surplus” to reduce school district M&O property tax rates as much as possible. Add to this spending restraint by local governments so they can use “surplus” funds to return to taxpayers by reducing their property tax rates until they are zero. This process of passing a frozen state budget, using 90% of surplus dollars to compress school district M&O property tax rates until they are zero, and having local governments eliminate the rest of their property taxes with surplus dollars above a new local spending limit will eliminate property taxes in Texas soon. This will help Texans own their property and have more liberty so that they have more opportunities to prosper.

Vance Ginn, Ph.D., is president of Ginn Economic Consulting and contributor to more than 15 think tanks, including Americans for Tax Reform, Texans for Fiscal Responsibility, and Texas Policy Research Initiative. Dr. Ginn was previously a lecturer at multiple higher education institutions, chief economist at the Texas Public Policy Foundation, and chief economist at the White House’s Office of Management and Budget. He earned his doctorate in economics at Texas Tech University. Follow him on X.com at @VanceGinn and get more of his research at vanceginn.com.

Texans for Fiscal Responsibility relies on the support of private donors across the Lone Star State in order to promote fiscal responsibility and pro-taxpayer government in Texas. Please consider supporting our efforts! Thank you!

Get The Fiscal Note, our free weekly roll-up on all the current events that could impact your wallet. Subscribe today!