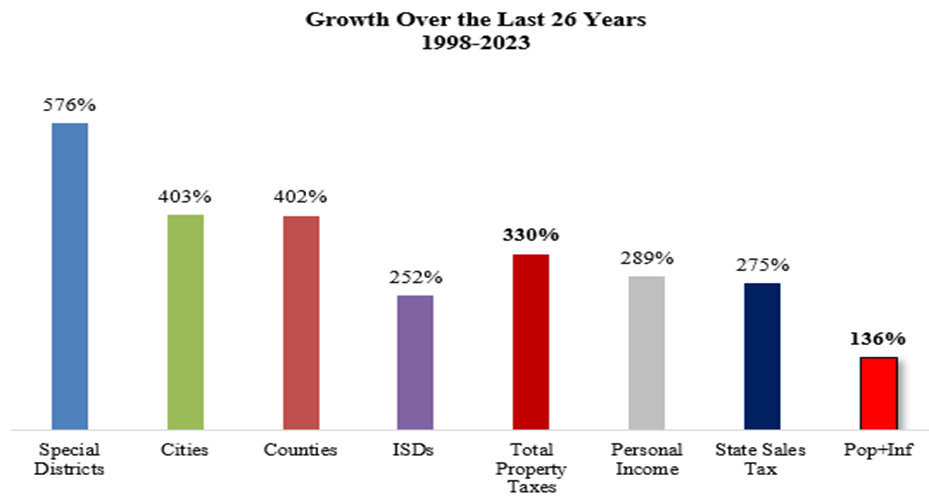

Property taxes are a financial burden that Texans can no longer afford to endure. Over the past 26 years, Figure 1 illustrates how property taxes have increased by an unsustainable 330%, far outpacing population and inflation growth of 136%.

Figure 1. Growth in Property Taxes and Economic Measures in Texas Since 1998

Source: Texas Comptroller’s Tax Levies and Rates, Biennial Property Tax Report, and Monthly State Revenue Watch, and Texas Legislative Budget Board

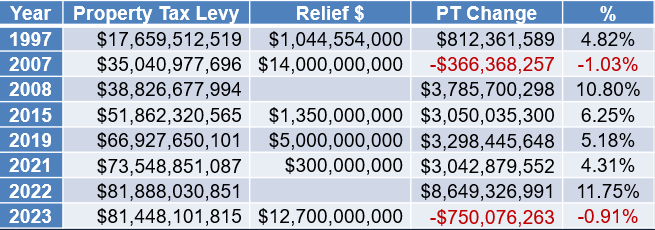

For Texans, this is not just an economic issue—it’s a question of fairness and freedom. Property taxes make homeowners perpetual renters, burden renters and businesses, and restrict economic opportunity. Despite six legislative attempts since 1997, Table 1 shows the structural problems driving property tax growth remain unaddressed and unresolved. Texans need bold, permanent solutions.

Table 1. Property Tax Growth and Relief Efforts in Texas Since 1997

Source: Texas Comptroller’s Tax Levies and Rates, Biennial Property Tax Report, and Texas Legislative Budget Board

Two pathways to finally eliminate property taxes include:

- Surplus-driven buydowns funded by limiting spending, or

- Redesigned tax system that swaps funding by increasing sales or other taxes.

Ultimately, Texas can achieve true homeownership and foster economic prosperity through spending restraint, transparency, and voter accountability.

The Problem: Why Property Taxes Must Go

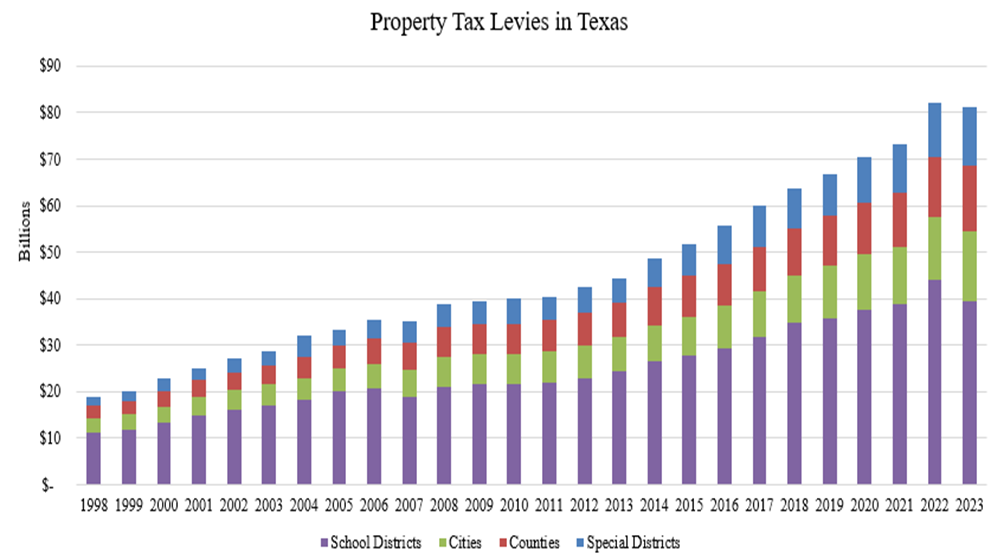

Property taxes are burdensome in both design and execution. Figure 2 highlights how property taxes have increased fourfold since 1998. This unchecked growth has created severe economic distortions and eroded true homeownership.

Figure 2. Property Taxes Have Quadrupled Since 1998

Source: Texas Comptroller’s Tax Levies and Rates and Biennial Property Tax Report

Uncontrolled Growth

Since 1997, property taxes in Texas have exploded, growing faster than the population and inflation combined. Special districts led the way with an astronomical 576% increase, followed by cities (403%) and counties (402%), as shown in Figure 1.

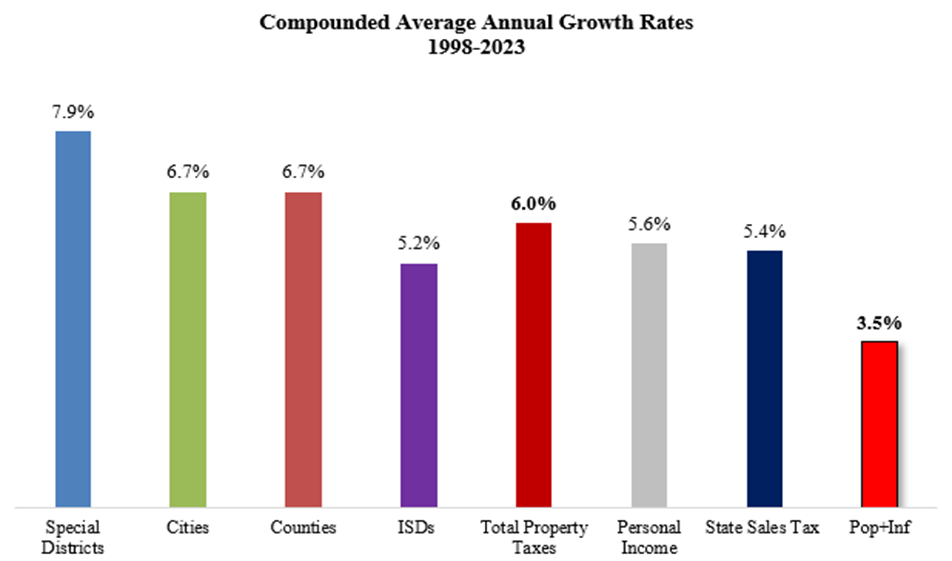

Figure 3 shows how property taxes increased by 6% on a compounded annual rate, which was 72% higher than the average Texan’s ability to afford them, as measured by the rate of population growth plus inflation.

Figure 3. Property Taxes in Texas Outpace Key Economic Measures

Source: Texas Comptroller’s Tax Levies and Rates, Biennial Property Tax Report, and Monthly State Revenue Watch, and Texas Legislative Budget Board

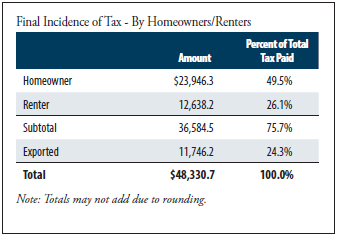

Property taxes affect all families who are homeowners, renters, and business owners, as noted in the Texas Comptroller’s 2023 report. Figure 4 from the Texas Comptroller’s Office shows that estimated school property taxes’ final incidence (i.e., burden) hits families across Texas.

Figure 4. School District Property Taxes Burden Families (2025 Amounts In Millions)

Source: Texas Comptroller’s Tax Exemptions and Tax Incidence Report

- Homeowners: Even after making mortgage payments, taxes continue to come in. If a homeowner fails to pay, the government can seize their property.

- Renters: Landlords pass property taxes down to renters, raising the cost of housing.

- Businesses: Higher property taxes discourage investment and reduce competitiveness.

Homestead Exemptions: A Misguided Solution

While well-intentioned, homestead exemptions, which exempt an amount from the appraised value for property taxes, are not the answer:

- Excludes Renters and Businesses: Relief only applies to homeowners, leaving families who are renters and business owners to carry a greater share of the spending burden. Everyone pays higher property tax rates than otherwise, making eliminating them more difficult.

- Locks People In: Exemptions incentivize homeowners to remain in their properties even if moving would better suit their needs.

- Loses Value Over Time: As property values rise, the relative value of a $100,000 exemption shrinks, rendering it ineffective over the long term.

A Lack of Accountability

Most local governments, except special purpose districts and some other small tax jurisdictions with a maximum of 8%, can raise property taxes by 3.5% on existing property (with no limitation on new property) without direct voter approval.

With these loopholes in current law, county and city taxes increased by over 10% last year. This lack of oversight enables runaway spending and taxes. To address this, all property tax increases above 0% must require voter approval, with a 0% growth rate unless explicitly approved by the public.

This means that as the County appraisal office does appraisals, the property tax rate determined by the local governing body must go down, so that the tax revenue (levy) collected doesn’t change from the prior period. This levy cap system makes appraisal caps or tax rate caps unnecessary, and the no-new-revenue rate is what the levy cap should be.

The limitation must be on the levy collected from all property taxes, which a strong spending limit that covers spending from all revenue, including property taxes, sales taxes, and other revenues, should ultimately do. This would make it less relevant where the tax revenue comes from as the spending and, therefore, taxes are held in check and hopefully reduced.

Pathway 1: Surplus-Driven Buydowns

The surplus-driven buydown approach systematically reduces property taxes over time by dedicating state budget surpluses to lowering tax rates until they are zero. This gradual method ensures that essential services remain funded during the transition.

How It Works

- Cap Local Tax Increases:

- Implement a 0% voter approval rate for local property tax increases. Voters must explicitly approve any proposed increase until they are eliminated.

- Limit State and Local Spending Growth:

- Cap state spending and local spending growth with a maximum rate of population growth plus inflation, providing higher surpluses over time.

- Dedicate State and Local Surpluses:

- Allocate annual state general revenue surpluses to buying down (i.e., compress) school district maintenance and operations (M&O) property tax rates, and local government surpluses to buying down their property tax rates, to zero.

- Phase Out Debt Taxes:

- Local governments have interest and sinking (I&S) taxes for debt purposes. In most cases, eliminate the largest of the two, M&O taxes, first, then I&S taxes.

Scenarios of Surplus Buydowns to Eliminate Property Taxes

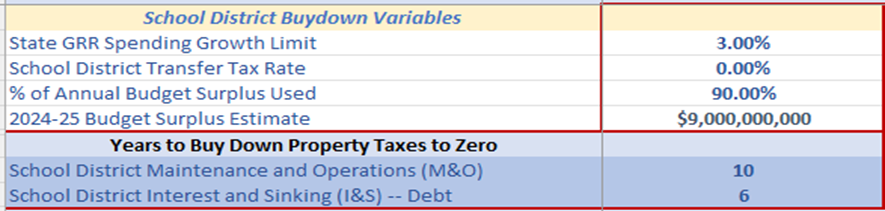

- Scenario A: State Surplus Buydown of School District M&O Property Taxes

- This scenario would take about 10 years to eliminate the school district M&O property taxes.

- Eliminating school district I&S property taxes with either state surplus or local surplus buydown could take another 6 years.

- This would effectively move 100% of funding government schools to state taxes (mostly sales taxes), thereby eliminating Recapture (Robin Hood), but it would not change local control under current law.

Table 2. Scenario A

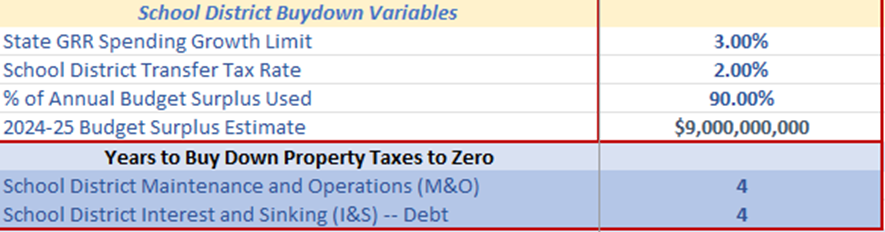

- Scenario B: Accelerated Buydown of School District M&O and I&S Property Taxes

- Assuming the 3% spending limit with a 90% surplus buydown and a 2% transfer tax rate on the sale of property, which would need a constitutional amendment, eliminating both could take about 8 years instead of the 16 in Scenario A.

Table 3. Scenario B

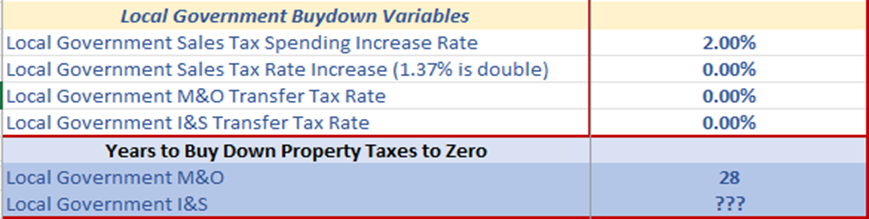

- Scenario C: Buydown of Other Local Government M&O Property Taxes

- Assuming a 2% spending limit on local governments with a surplus buydown using local taxpayer dollars, mostly from sales taxes, eliminating local government M&O property taxes for cities, counties, and special purpose districts could take 28 years, even longer for I&S. Of course, a transfer tax on the sale of property would help speed up these elimination periods.

Table 4. Scenario C

Pros of Surplus Buydown Method

- Reduces Texans’ Tax Burden: Fund the surplus buydown through fiscal restraint from strict state and local spending limits would reduce future taxes and the government’s size and scope.

- Incremental, Transparent Progress: Provide incremental, immediate annual relief for taxpayers and prevent backdoor tax increases by requiring voter approval.

Cons of Surplus Buydown Method

- Reliance on Political Decisions: Could depend on politicians consistently providing surplus generation from spending restraint.

- Requires Coordination: Maintain fiscal discipline by state and local governments, which has been difficult to nonexistent after multiple attempts at reforms.

Pathway 2: Sales Tax (Swap) Redesign

A redesigned tax system in Texas would swap sales taxes for property taxes, preferably with a strong spending state and local spending limit and surplus buydown to reduce sales and other taxes. This approach depends on:

- broadening the sales tax base while also,

- keeping sales tax rates competitive.

How the Redesign Works

- Expand the Sales Tax Base:

- Include currently exempt goods and services, such as boats, airplanes, and professional services, in the tax base

- Maintain exemptions for essentials like groceries and prescription medications (though the sales tax rates could be lower if these items are taxed).

- According to the Texas Comptroller, Table 5 shows an estimated $42.2 billion in sales tax exemptions, $12.9 billion in exclusions, and $354.7 million in discounts in 2023, for a total of $55.5 billion.

Table 5. Narrowing Factors to the Sales Tax Base

Source: Texas Comptroller’s Tax Exemptions and Tax Incidence Report

- Adjust State and Local Sales Tax Base and Rates:

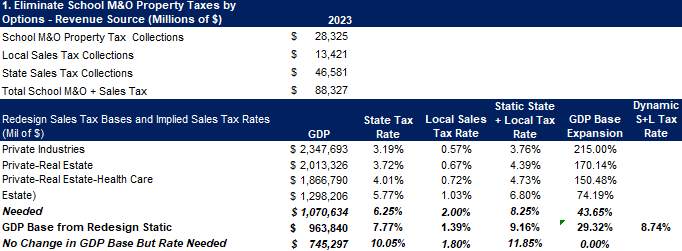

- The state replaces school district M&O taxes (see Table below):

- Requires a sales tax rate of 11.85% with the currently taxed GDP base of $745.3 billion or an expansion of the base by 44% of $1.07 trillion to keep the state and local sales tax rate at 8.25%. However, by expanding the base by 29% to $963.8 billion while not double-taxing items, the sales tax rate would increase to 9.16% (7.77% for state rate and 1.39% for local rate), which would not be the highest in the country, and nearly half of the property tax would be eliminated.

- Table 6 provides the sales taxes needed to replace school district M&O property taxes with different GDP bases, static state and local sales tax rates, GDP base expansion, and dynamic state and local tax rates.

- The state replaces school district M&O taxes (see Table below):

Table 6. Redesign Tax System With Higher Sales Taxes for the State to Eliminate School District M&O Property Taxes

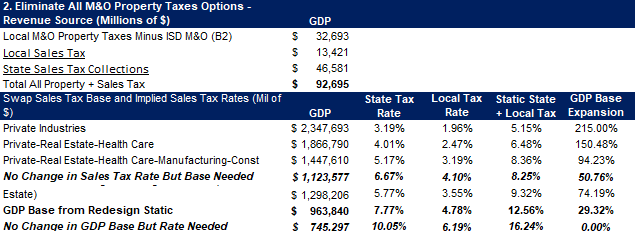

- The state replaces school district M&O, and locals replace their M&O (Table 7)

- Requires a static state and local sales tax rate of 16.24% without expanding the sales tax base to cover school district, city, county, and special purpose district M&O property taxes. To keep the same 8.25% combined sales tax rate, the GDP base for sales taxes would need to expand by 51%. These approaches are politically difficult and would make the state highly uncompetitive with neighboring states.

- The better approach would be to expand the sales tax base by at least 29% for a state and local sales tax rate of 12.57%, with the state rate at 7.77% and the local rate at 4.8%. This sales tax rate remains high but could be doable given that 75% of property taxes would be eliminated, and just the I&S property taxes would remain.

Table 7. Redesign Tax System With Higher Sales Taxes for the State to Eliminate School District M&O Property Taxes and Locals to Eliminate Their M&O Property Taxes

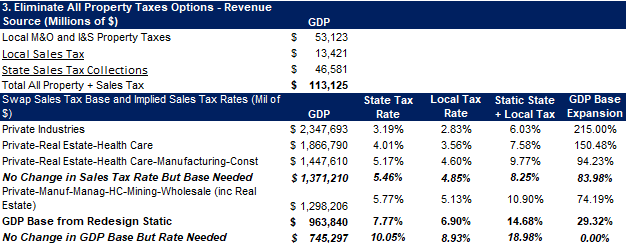

- The state replaces school district M&O, and locals replace M&O and I&S (Table 8):

- This requires a state and local sales tax rate of 18.98% without expanding the sales tax base of $745.3 billion to cover school district, city, county, and special purpose district M&O and I&S property taxes along with the sales taxes collected at the state and local levels. To keep the same 8.25% combined sales tax rate, the GDP base for sales taxes would need to expand by 84% to $1.37 trillion. These aren’t politically or economically possible and would make the state highly uncompetitive.

- The better approach would be to expand the sales tax base by at least 29% to $963.8 billion for a state and local sales tax rate of 14.68%, with the state rate at 7.77% and the local rate increasing to 6.9%. This sales tax rate is likely too high. Still, it would eliminate all property taxes in Texas, and the dynamic rate from more economic growth from this approach would bring the combined rate down closer to 13%, which would be the highest in the country but without any taxes on property.

Table 8. Redesign Tax System With Higher Sales Taxes for the State to Eliminate School District M&O Property Taxes and Locals to Eliminate Their M&O and I&S Property Taxes

- Ensure Spending Restraint, Transparency, and Accountability:

- Avoid taxing intermediate goods to prevent double taxation, do not allow any future increases in sales tax rates, and

- Use the surplus buydown approach with a strict spending limit discussed above to reduce sales tax rates, franchise tax rates, or other taxes.

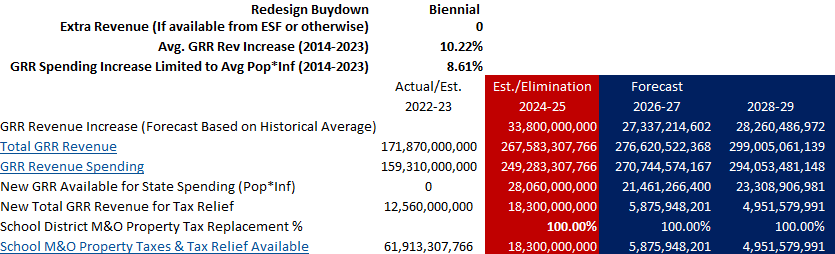

- Table 9 shows the surplus buydown biennially using historical averages for the school district M&O property tax elimination with a redesigned tax system. This property tax would have been eliminated in 2024-25, and the surpluses of $5.9 billion in 2026-27 and after that could be used to reduce other tax rates.

Table 9. Redesign Tax System with Surplus Buydown Approach

Pros of Tax System Redesign

- Immediate Relief: Fully replaces some or all property taxes in one reform, as spending is restrained and there is no need for revenue-neutral redesign.

- Economic Efficiency: Encourages investment and entrepreneurship by taxing consumption, not ownership, and supports greater economic growth.

Cons of Tax System Redesign

- May Not Reduce the Tax Burden: Increasing sales taxes to eliminate property taxes does nothing to reduce state or local government spending or decrease the future tax burden unless it is a net tax cut, which, combined with spending less, is preferable.

- Implementation Complexity: Requiring significant effort initially but possibly needing much less than other efforts later on.

Rejecting a European-style VAT

Some suggest implementing a Value-Added Tax (VAT) instead of a broader sales tax to fund the property tax swap. This would be a mistake:

- Hidden Costs: VATs embed taxes at every production stage, obscuring the true tax burden for consumers.

- Complexity: Administrative and compliance costs are much higher than a simple sales tax.

- Economic Distortions: VATs disproportionately harm lower-income households by raising the cost of goods.

Texas must avoid adopting European-style tax systems that stifle economic freedom and growth.

Recommendations for Legislators

To ensure success, any plan to eliminate property taxes must include the following:

- Voter Approval for Any Property Tax Increase

- Require voter approval for any increases in local property taxes (or sales taxes).

- Focus on Rate Compression

- Focus on permanent tax elimination through lowering property tax rates instead of temporary relief measures, like the homestead exemption, that exclude families who are renters or business owners.

- Cap Spending Growth

- To reduce the size and scope of government and support consistent surpluses, limit state and local spending increases to, at most, the rate of population growth plus inflation, with surpluses being used to lower tax rates.

- Pass Constitutional Amendment: After eliminating property taxes, pass a constitutional amendment so they can never return.

Conclusion: A Bold Vision for Texas

Texas must move beyond temporary fixes and fundamentally transform the state-local tax system. Whether through surplus-driven buydowns or a redesigned sales tax, the result will be a freer, fairer, and more prosperous state.

Table 10. Comparison of Surplus Buydown and Tax System Redesign Approaches to Eliminate Property Taxes in Texas

| Aspect | Surplus Buydown | Tax System Redesign |

| Timeline | Gradual (4–10 years) | Immediate (1–2 years) |

| Fiscal Discipline | Relies on limiting spending | Relies on making reforms |

| Economic Impact | Gradual relief encourages growth | Immediate boost to economy |

Texans deserve true property ownership, economic opportunity, and a government that operates within its means.

Let’s end property taxes and empower Texans to prosper. The time to act is now.

Texans for Fiscal Responsibility relies on the support of private donors across the Lone Star State in order to promote fiscal responsibility and pro-taxpayer government in Texas. Please consider supporting our efforts! Thank you!

Get The Fiscal Note, our free weekly roll-up on all the current events that could impact your wallet. Subscribe today!