Executive Summary

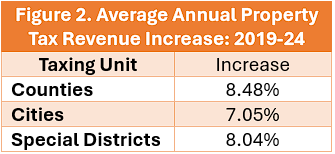

Texas’ political leaders claim they will spend $51 billion (of taxpayer money) the next two years on public schools to provide property tax relief to homeowners, small businesses, and other landowners. Yet over the last six years of legislative efforts to reduce the property tax burden, property taxes have increased $23.6 billion. During that time, the annual growth rate of property taxes for counties is 8.48%, cities 7.05%, and special districts 8.04%. The Legislature’s efforts to provide property tax relief are not working.

Gov. Greg Abott has asked the Legislature to “consider and act upon … [l]egislation reducing the property tax burden on Texans” during the 1st Called Special Session that began this week. However, instead of throwing good money after bad by offering more of the same “relief,” the Legislature should first do what it takes to stop local governments from undoing its efforts at relief by putting strong limits on the growth of city, county, special district, and school district property tax revenue.

There are two simple steps to lasting property tax relief in Texas. First, transparency: make the no-new-revenue property tax rate result in no new revenue for each local taxing entity. Second, accountability: reset the voter-approval property tax rate to equal the no-new revenue rate. If a local government or school district wants to increase their property tax revenue, it can ask voters; if the voters reject the increase, the taxing entity will have to make do with what it spent last year. If the voters approve the increase, the absolute maximum increase should be the lesser of 7.84% (see explanation below) or a three-year trailing average of population growth plus inflation.

Once these limits are put in place during the current special session, the Legislature should then devote 100% of budget surpluses to completely eliminate school property taxes. Then turn its attention to cities, counties, and special districts.

No Tax Relief (Property or Otherwise) for Texans Over the Last Seven Years

Pressured by Texans who were tired of seeing annual property taxes hikes making homeownership increasingly unaffordable, the Texas Legislature in 2019 began efforts in earnest to address the problem. Despite increasing spending on public education by billions of dollars over the last four sessions (by some estimates up to $51 billion) in an attempt to provide tax relief to Texans, their efforts have failed.

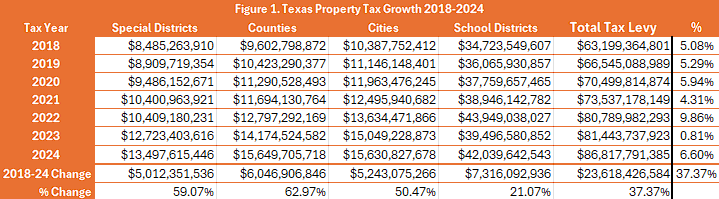

Figure 1 shows that property taxes have increased by $23.6 billion during this time. The reason why is simple. Local governments and school districts continue to rapidly increase property taxes to pay for runaway spending.

City property taxes are up more than 50% since the Legislature began its efforts. Special purpose district taxes are up 59%. County taxes are up 62%. School district property taxes are up only $7.3 billion and 21%. But if you take into account the reported $51 billion of state revenue being spent to make up for lower school property taxes, school spending supported by the local and state tax revenue is up as much as $58.3 billion, a 173% increase. And despite more property tax “relief” from the Legislature in its 2025 regular session, property taxes are expected to increase at least another $2 billion this year.

The truth is that there has been no property tax relief for Texans over the last seven years; unless one believes that a $23 billion increase in property taxes has somehow relieved weary, overtaxed Texans who are concerned about how much longer they can afford to live in their homes. For Texans overall, the tax state and local burden they are paying to support local governments and schools has significantly increased during this time.

The Path to True Property Tax Relief—Limiting Revenue and Spending Growth by Local Governments

Over the last seven years Texans have learned a very expensive lesson about property taxes: government spending is the problem. Throwing money at school districts without slowing or stopping local government spending growth has increased our overall tax burden. If we want lower taxes, we must reduce government spending.

There are two ways to accomplish this. First, by requiring local governments to reduce spending. Second, by cutting off local government revenue growth. Fortunately, Gov. Greg Abbott has put both options on the 1st Called Special Session of the 89th Texas Legislature that began this week.

One item is his proclamation convening the special session deals directly with this problem. He asked the Legislature to “consider and act upon … [l]egislation reducing the property tax burden on Texans and legislation imposing spending limits on entities authorized to impose property taxes.” Another paper by Texas for Fiscal Responsibility will examine what can be done with local government spending limits. This paper will focus on how the Texas Legislature can reduce or stop the growth of local government property tax revenue.

Existing Revenue Limits are Broken

In 2019, the Texas Legislature attempted to impose limits on the growth of property tax revenue. They adopted a no-new-revenue rate for cities, counties, schools, and special districts. They also imposed taxpayer-approval rates that could not be exceeded without a public vote. The taxpayer-approval rates require a public vote if property tax revenue would exceed the no-new-revenue rate by 3.5% for cities, counties, and certain special districts, 2.5% for school districts, and 8% for other special districts. However, both the no-new-revenue rate and the taxpayer-approval rate are full of exemptions that essentially make the limits worthless to taxpayers who are struggling under ever increasing property tax burdens.

The No-New-Revenue Rate

According to the Texas Comptroller, the no-new-revenue rate for property taxes is the “tax rate that would produce the same amount of taxes if applied to the same properties taxed in both years.” While this is correct, the no-new-revenue rate misleads most Texans because the Texas Legislature has provided a number of exemptions to the no-new-revenue rate that allows a taxing unit to substantially increase its revenue above the amount it received in the previous year. These exemptions include:

- Revenue from New Development. Increased revenue from new development on properties in the last year that increased their appraised value is not counted in the no-new-revenue rate calculations.

- State Criminal Justice Costs. Counties are allowed to increase their no-new revenue rates by the amount needed to produce additional revenue to pay for spending that covers the cost of keeping inmates in county-paid facilities that have already been sentenced to state jail or prison facilities.

- Indigent Health Care Costs. Taxing entities are allowed to increase their no-new revenue rates by the amount needed to produce additional revenue to pay for certain spending on indigent health care.

- Indigent Defense Expenditures. Counties are allowed to increase their no-new revenue rates by the amount needed to produce additional revenue to pay for spending on a public defender’s office and providing appointed counsel for indigent individuals in criminal or civil proceedings.

- County Hospital Expenditures. Counties and cities are allowed to increase their no-new revenue rates by the amount needed to produce additional revenue to pay for the costs of operating a hospital owned or leased by a county or a county and city.

The Voter-Approval Rate

Local governments and school districts that wish to exceed the voter-approval tax rate must call an election in which a majority of voters must approve the higher rate. However, much like with the no-new-revenue rate, the Legislature has put exemptions into law that allows taxing entities to exceed the voter approval limits in statute. The exemptions are:

- Disaster Relief. Current law allows a taxing unit to increase its tax revenue up to 8% in a single year if any part of the taxing unit is located in an area declared a disaster area without seeking approval through a public vote. Legislation passed this year changes this to allow a taxing unit to exceed the voter approval limit by the revenue needed to pay for the estimated costs “essential assistance” and removal of debris or wreckage in the taxing unit.

- Pollution Control Expenditures. Political subdivisions of this state are allowed to increase their voter-approval tax rates by the amount needed to produce additional revenue to pay for pollution control equipment that is necessary to meet the requirements of a permit issued by the Texas Commission on Environmental Quality

- “Unused” Increment Revenue from Previous Years. Taxing entities are allowed to exceed their voter-approval tax rates to “recapture” revenue anytime during the previous three years where an entity’s tax rate was less than the maximum allowed under the voter approval tax rate.

As Table 1 and Table 2 show, these exemptions, loopholes, or whatever they might be called, have led to property tax increases far above the paper limits in Texas law. For instance, in 2018, property tax revenue for counties was $9.6 billion. In 2024, county property tax revenue had increased by $6 billion to $15.6 billion, an average annual increase of 8.48%, more than double the statutory 3.5% voter-approval rate. For cities, over the same period revenue increased by $5.2 billion from $10.4 billion to $15.6 billion, an average annual increase of 7.05%, just over double the voter-approval rate. The average annual increase for special districts is 8.04%, an increase of $5 billion since 2018. There have been instances where voters have approved exceeding the voter-approval rate, but a large part of the increase above the statutory rates is due to the exemptions in the no-new-revenue and voter-approval tax rates.

Limiting Property Tax Revenue Growth in the 1st Called Special Session

If the Texas Legislature is going to stop the runaway growth of property taxes, two major reforms must be made during the current 1st Called Special Session. They are:

Transparency – Make the No-New-Revenue Rate Result in No New Revenue

As we’ve noted, the current limits on property tax increases are meaningless. There is no discernable relationship between the limits and the amount of property tax increases Texans experience every year. To fix this, transparency is needed. This entails first eliminating all of the exemptions to the no-new-revenue rate. This would result in the no-new-revenue rate actually being the rate that produces no new revenue for taxing entities. Thus, the limits that trigger voter approval would actually reflect the increases in revenue for the taxing entity. The 3.5% limit for cities and counties would reflect a 3.5% increase in property tax revenue instead of the current average of around 8%.

Accountability – Reset the Voter-Approval Rate to 0%

Most Americans think that government is too big and should be smaller and provide less services; this includes 79% of Trump supporters. Yet the current limits on property tax revenue growth allow Texas local governments to grow, on average, by almost 8% per year. There may be reasons to allow certain governments to grow by certain amounts at different times. But there is no reason that the growth should not be subject to the approval of Texas voters. This means both the current exemptions and growth limits in current law should be eliminated. This would make the voter-approval rate identical with the no-new-revenue rate.

If school districts and local governments want to increase spending, let them ask the voters. After all, it is the voters’ money that is being spent. If voters do approve the increase, the absolute maximum increase in any year should be the lesser of the average of population growth plus inflation for the three years prior to the property tax year in question, or 7.84%, the average annual property tax revenue increase for special districts, cities, and counties since growth limits have been in place (from 2018 through 2025).

Conclusion

The Legislature has spent billions of dollars of state taxpayer money on school districts in the name of property tax relief. Yet, Texas taxpayers have still experienced increasing property tax bills because of the rapid growth of spending at the local level.

Rather than spending more taxpayer money on fruitless relief efforts, the Texas Legislature should slow or stop the spending growth by putting strong limits on property tax revenue increases. Once this is done, the Legislature can return to using budget surpluses to permanently reduce property taxes.

Texans for Fiscal Responsibility relies on the support of private donors across the Lone Star State in order to promote fiscal responsibility and pro-taxpayer government in Texas. Please consider supporting our efforts! Thank you!

Get The Fiscal Note, our free weekly roll-up on all the current events that could impact your wallet. Subscribe today!